Understanding Trust Bank Financial Statements

Trust bank balance sheet

- (1)

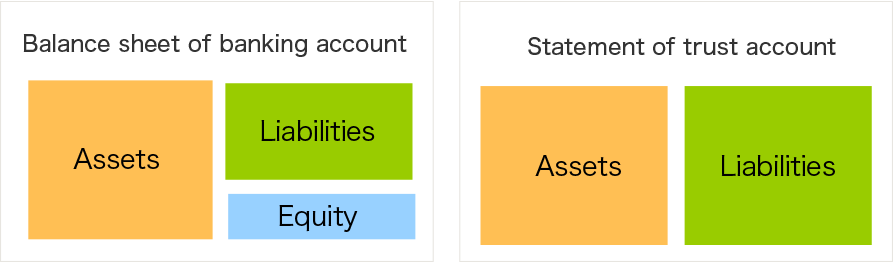

Trust banks have two balance sheets: one for the banking account and one for the trust account. The balance sheet that records the trust bank's own capital, fund management, and financing is the banking account, while the trust account represents the balance sheet concerning the trust assets entrusted to the bank by settlors and administered, managed and disposed on behalf of beneficiaries in line with the purpose of trust contracts.

- (2)

The results (profit or loss) of administration, management and disposition in the trust account are returned to the beneficiaries, less trust fees collected by the trust bank. In principle, the results have no impact on the banking account. However, loan trusts and jointly-managed money trusts are the exception; they are subject to principal-guaranteed contracts and covered by deposit insurance. As such, loan trusts and jointly-managed accounts have their own balance sheets, which are released, and together with the banking account, are referred to as the "three accounts." It is standard practice for trust banks to manage financial risks on the basis of these three accounts.

- Note:New subscriptions to loan trusts have been suspended, so their impact on the size of balance sheets and financials is limited.

- Note:

- (3)The trust assets balance table released as the trust account balance sheet shows the balance of entrusted assets for each type of trust in the liabilities section and assets (loans and bills discounted, securities, real estate, monetary claims, etc.) held as trust assets in the assets section. It should be noted that there are various trust products also listed as monetary trusts. For example, there are some in which trust banks possess discretionary power over investments ( jointly-managed and individually operated designated money trusts, etc.) and some in which they do not (specific money trusts, etc.). The trust bank compensation system for these products also differ. In addition to monetary trusts, trust banks have discretionary power over investments in loan trusts and pension trusts, but no such authority in investment trusts and securities trusts.

Trust bank income statement

Trust banks release statements of income for the banking account. The main items that comprise net business profit before credit costs—the equivalent of operating profit at an ordinary company—are as follows.

- (1)Trust Fees

- (2)Net Credit Cost of loan trusts and JOMT accounts

- (3)Net Interest Income

- (4)Net Fees and Commissions

- (5)Net Trading Income

- (6)Net Other Ordinary Income (gains or losses on sales of bonds, net gain or loss on foreign exchange transactions, net income or expense on derivatives other than trading or hedging)

- (7)Gross Business Profit: (1)+(3)+(4)+(5)+(6)

- (8)General and Administrative Expenses

- (9)Transfer to general allowance for loan losses

- (10)Net Business Profit: (7)-(8)-(9)

- (11)Net Business Profit before Credit Costs: (10)+(2)+(9)

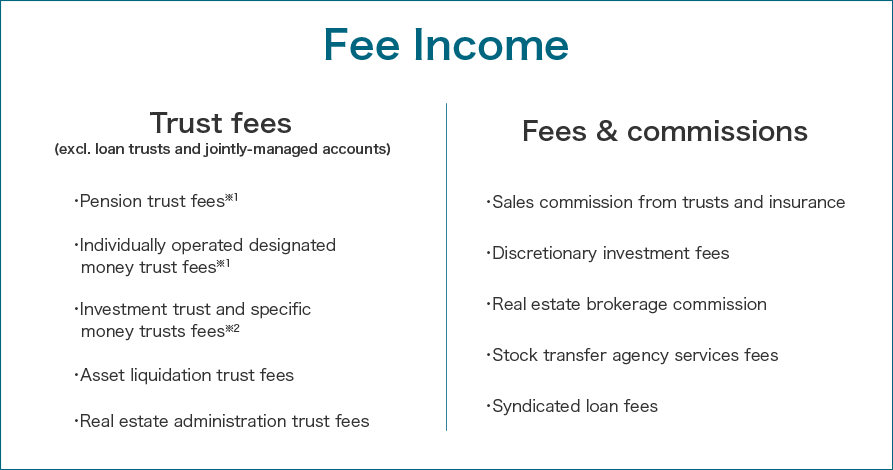

Trust bank fee income: trust fees and fees & commissions

In a broad sense, there are two types of fee income for financial accounting purposes at trust banks: trust fees and fees & commissions. The payments a trust bank receives in accordance with trust contracts are booked as trust fees, while payments and fees collected under general services agreements are booked as fees & commissions. However, because trust fees for loan trusts and jointly-managed accounts are of a similar business nature to banking operations (deposits and loans), they are generally excluded from fee income. At the SuMi TRUST Group they are booked under interest related earnings.

- *1Administration and management fees from monetary trusts in which the bank has discretionary power over investments

- *2Administration fees only from monetary trusts in which the bank has no discretionary power over investments